The Calculus of Freedom: Deconstructing the Snowball and Avalanche Debt Repayment Strategies

In the landscape of personal finance, the journey out of debt is a critical path to economic sovereignty. Among the myriad of strategies available, two have emerged as dominant frameworks: the debt snowball and the debt avalanche. While both aim for the same destination—a zero balance—their methodologies are fundamentally different, pitting the rigorous logic of mathematics against the powerful undercurrents of human psychology. An in-depth analysis reveals that the “best” method is not a universal prescription but a deeply personal choice contingent on an individual’s financial circumstances, behavioral tendencies, and long-term objectives. The core of the debate lies in a single question: Is it more effective to be motivated by quick, tangible victories or by the knowledge of maximum financial efficiency?

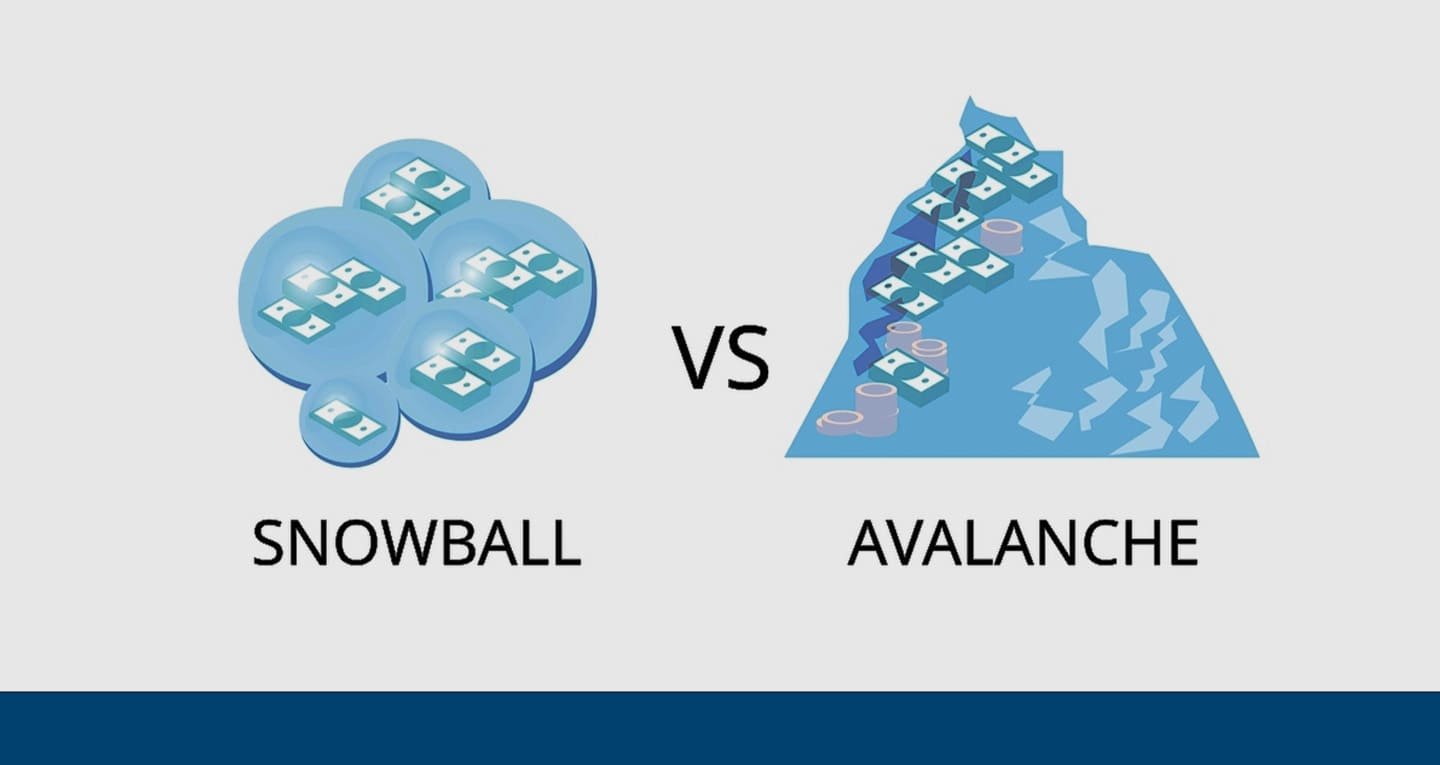

The Debt Avalanche: A Testament to Mathematical Optimization

The debt avalanche method is the embodiment of financial prudence, a strategy built on the unassailable logic of interest rate optimization. [1][2] This approach mandates that after making minimum payments on all outstanding debts, any surplus funds are directed toward the loan with the highest annual percentage rate (APR). [3][4] Once that debt is extinguished, the entire payment amount is reallocated to the debt with the next-highest interest rate, creating a cascading effect. [2] The primary and most compelling advantage of this method is its cost-effectiveness. By systematically eliminating the most expensive debts first, individuals minimize the total interest paid over the life of their loans, which often translates into becoming debt-free sooner. [5][6] For example, consider a scenario with a $10,000 credit card debt at 18.99% APR and a $9,000 car loan at 3.00%. The avalanche method would aggressively target the credit card, potentially saving hundreds or even thousands of dollars in interest compared to other strategies. [7] This makes it the superior choice for individuals who are analytical, disciplined, and motivated by long-term financial gains and efficiency. [8] The strategy, however, is not without its challenges. Its primary drawback is behavioral; if the debt with the highest interest rate also has a large balance, it can take a significant amount of time to pay it off, delaying the gratification of a “win” and potentially leading to a loss of momentum. [5][9]

The Debt Snowball: Harnessing the Power of Behavioral Economics

In stark contrast, the debt snowball method, famously championed by financial expert Dave Ramsey, prioritizes psychology over pure mathematics. [10][11] This strategy involves listing all debts from the smallest balance to the largest, regardless of interest rates, and focusing all extra payments on the smallest debt first. [3][4] Once the smallest debt is eliminated, the payment amount is “rolled over” to the next-smallest debt, creating a growing “snowball” of payments. [12] The core strength of this method lies in its powerful motivational impact. Achieving a quick win by paying off a small debt provides a significant psychological boost and a tangible sense of progress, which can be crucial for maintaining long-term commitment. [10][13] Research from institutions like Northwestern’s Kellogg School of Management and studies published in the Harvard Business Review have supported this, finding that consumers who tackle small balances first are more likely to eliminate their overall debt because the feeling of progress is a powerful motivator. [11][14] This “debt account aversion,” or the psychological preference for closing accounts, makes the snowball method highly effective in practice, even if it’s not the most mathematically optimal. [15] The most significant disadvantage, however, is the potential for higher overall interest costs, as high-interest debts may be left to accrue interest for longer periods. [13][16]

Strategic Synthesis: From Theory to Real-World Application

The binary choice between snowball and avalanche often oversimplifies the complex reality of personal finance. The most sophisticated approach may, in fact, be a hybrid model that leverages the strengths of both. [5][9] An individual could begin with the snowball method to quickly eliminate one or two small debts, generating momentum and building confidence. [4][9] With that motivational foundation established, they could then pivot to the avalanche strategy, redirecting their now-larger “snowball” payment to the debt with the highest interest rate, thereby maximizing interest savings for the remainder of their journey. [5][17] This blended approach acknowledges the critical insight that personal finance is “20 percent head knowledge and 80 percent behavior,” a concept Ramsey often highlights. [11] The decision is also contextual. If the interest rates across a person’s debts are relatively similar, the financial benefit of the avalanche method diminishes, potentially making the motivational edge of the snowball method more valuable. [18][19] Conversely, for someone with a significant amount of high-interest credit card debt, the cost savings from the avalanche method are too substantial to ignore. Ultimately, the journey to financial freedom is not about finding a single “correct” answer but about creating a sustainable, personalized plan. It requires a clear-eyed assessment of one’s debts, an honest understanding of one’s own psychological drivers, and the discipline to consistently execute the chosen strategy. [8]